Income and Expenses

Recording income and expenditures is a first step that you might think of about when you start managing your personal finances. However, not all expenditures are equal. Paying off debts or buying stocks, bonds, etc. decrease the amount of money available, but also decrease liabilities or increase assets, while living expenses simply decrease the amount of money available. So, you should split expenditures into transfers, which may have a long-term value, and expenses, which are payments for thinks that are consumed.

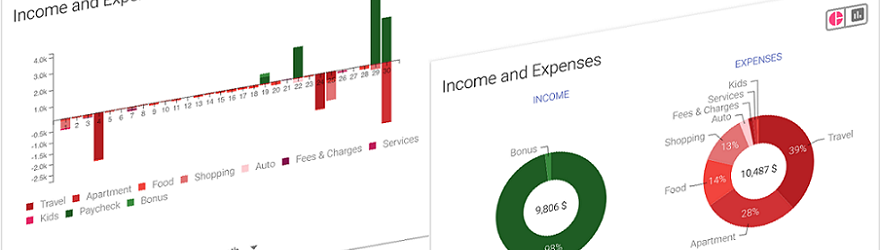

In MoneyBench app we use transactions for tracking income, expenses and transfers, but you can create a cash in/outflow sheet in Excel or Numbers:

| Income | Jan | … | Dec |

|---|---|---|---|

| Net salary/wages | |||

| Interest/dividend income | |||

| Tax refunds | |||

| Gifts/grants | |||

| Total income |

| Expenses | Jan | … | Dec |

|---|---|---|---|

| Rent | |||

| Auto expenses | |||

| Food | |||

| Utilities | |||

| Donations | |||

| Taxes | |||

| Vacations | |||

| Entertainment | |||

| Interest payments | |||

| - Credit card | |||

| - Loan | |||

| - Mortgage | |||

| Total expenses |

| Transfers | Jan | … | Dec |

|---|---|---|---|

| Balance pay-offs | |||

| - Credit card | |||

| - Loan | |||

| - Mortgage | |||

| Stocks, bonds, etc. | |||

| Deposits | |||

| Totals transfers |

| Jan | … | Dec | |

|---|---|---|---|

| Cash surplus/deficit |

The cash in/out flow sheet will show whether you were successful in the given period of time. If you weren't able to save money or decrease your liabilities, you should find a way to increase your income or decrease your expenses.

Income is usually the less flexible part because it usually requires long term investments such as finding a better position or even changing the entire career path. You should have enough financial capacity before making such serious moves. It is much easier to forsake vacations and entertainment like many people do, but usually it is better to review your food preferences, auto expenses and service subscriptions.